Its preparation should involve the managers who will assume authority to ensure that they understand the objectives, think they are reasonable, and are committed to their attainment.

Budgeting cannot take the position of management but it is only an instrument of management. A budget, on the other hand, involves a commitment to a forecast to make an agreed-on outcome happen. Good budgetary control necessitates establishment of accounting procedures to record actual operations in terms of sales, income, production, etc.

Account Disable 12. Both the top-down and bottom-up approaches have advantages whose importance varies in accordance with the nature of the business and the companys stage of development (see Exhibit 1).

Budget preparation should begin as near the start of the period as possible while still allowing enough time to do a thorough job. Various budgeting models continue to be commonly used and fall predominantly into the following categories: (1) line-item, or "traditional," budgeting; (2) performance budgeting; (3) program and planning ("program") budgeting; (4) zero-based budgeting (ZBB); (5) site-based budgeting; and (6) outcome-focused budgeting. Should they start the process with tightly specified objectives? Budgetary control attempts to show the plans in financial terms. Large companies use budgets for annual planning and then for control to ensure that operations go according to the original plan. The cookie is used to store the user consent for the cookies in the category "Analytics".

The top-down approach allows the owner-manager and others at the top to put forward their comprehensive views of the organization and its economic and competitive environments.

Is corrective action needed; should it be applied? By the end of this book, we should all agree that budgeting is a necessity not a luxury.

The company sells three-fourths of its products to American manufacturers of electrical and electronic equipment and the remainder abroad.

Management prepares an annual budget, composed of four quarterly budgets of thirteen weeksthe original budget. Every six months it revises the annual budget for the remaining six months and adds on a new six-month budgetthe revised budget. At the end of each month, it also prepares a revised forecast for the next 13 weeks, altering the existing quarter budget when necessary, and adding an additional month.

Perhaps this is why the extensively integrated smokestack industries have found it so difficult to adapt to the rapidly changing environment in which they find themselves. A budget can support delegation better if the need for performance feedback is considered in its design and construction.

He concludes that large companies concerned about operational efficiency should focus on the coordination and control aspects of budgeting while small and innovative companies should be concerned with planning aspects. Top management sets forth in broad terms, and sends to the operating-unit managers, an overview of the environment, the corporate goals for the year, and the resource constraints. WebThe budget process has three main phases, each of which is related to the others: 1. Consistent with the evaluation objective, government budgeting is becoming increasingly outcome focused. 3. This wasteful way of using budgets overlooks important managerial objectives that [], A version of this article appeared in the.

This IMF working paper examines the budgetary powers of the legislature under different forms of government.

The HUB, Sy. 3.

Consider, for example, a company with sales, fixed costs, and variable costs as shown in the table. Usually, however, the strategic plan precedes the budget and the linkage is less pronounced. Number 8/2 & 9, Sarjapur Road, Bengaluru, Karnataka- 560 103, Software Service

Despite its substantial benefits, site-based budgeting also has limitations. Occasionally a company uses a budget with stretch in it for motivating performancesales, for instanceand a more realistic budget for planningexpected sales, for example. The salespeople, in turn can use a budget as an excuse to call on their customers and talk to them about their advertising needs and plans. If fixed expenses remain within budget, the departments profits rise and fall by the same amount as their contributions to overhead and profit. As this example shows, budgets can be used both for planning (Number 1) and for control (Number 2), although the same budget is not always optimal for both purposes. In addition, many governmental organizations use a variety of hybridized versions to address their specific needs. 3.

Deviations from predetermined plans are brought to notice through variance analysis and corrective action is stimulated by reports, statements and personal contacts.

The bottom-up approach, on the other hand, makes use of operating managements detailed knowledge of the environment and the marketplace, knowledge that is available only to those who are involved on a daily basis.

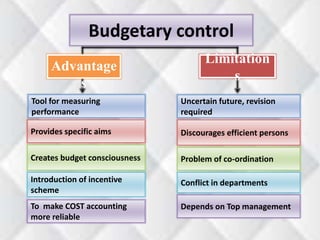

Thus, it leads to smooth production chains. Besides planning, budgetary control should provide a basis for, measuring performance and exercising control-control means noting when expenditures fall outside the budget estimates, tracing down the cause of such variation and taking necessary corrective action. This conceptual framework includes the practices of explicitly projecting the long-term costs of programs and evaluating different program alternatives that may be used to reach long-term goals and objectives. For a successful planning budget, compensation should be based on other criteria, such as current achievements compared with previous ones, profits, return on investment, or other agreed-on objectives.

If he feels that his department is falling behind than what was expected of, he prepares a report and reveals the points of difficulty so that the unfavourable situation may be analyzed and improved by taking suitable corrective actions. Necessary cookies are absolutely essential for the website to function properly. We also share information about your use of our site with our social media, advertising and analytics partners who may combine it with other information that youve provided to them or that theyve collected from your use of their services. Line-item budgeting is still the most widely used approach in many organizations, including schools, because of its simplicity and its control orientation.

WebWe call the overall budgeting process budgetary control; and the reason for using it is to help managers control the activities in their part of their organisation.

Budget should analyze all the factors affecting the sections/departments and the business as a whole.

WebThe budgeting process is an essential component of management control systems, as it provides a system of planning, coordination and control for management.

Budgeting is closely connected with control.

Budget revision, however, is a highly controversial issue. Budget coordinates the efforts of all the sections, (e.g., sales, production, etc.)

Every functional executive knows what was expected of his department and presently where his department stands. Budgeting is a structured format of goals and However, performance budgeting is limited by the lack of reliable standard cost information inherent in governmental organizations.

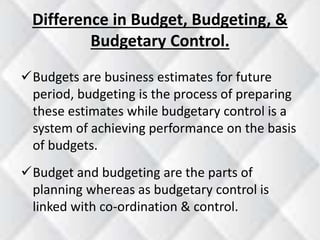

WebDistinguish between Budgets and Budgetary Control A budget is a formal written statement of managements plans for a specified future time period, expressed in financial terms.

Budgetary control should watch the progress of achievements of the business enterprise and evaluate policies of the management.

3.

For a discussion of the different stages of development of small companies, see Chap. Most companies use budgets to evaluate, to some extent, managers performance. 12.

This is the measure used to evaluate overall company performance, particularly that of public corporations. The following terms are used frequently throughout the Governors Budget, the Governors Budget Summary, the annual Budget (Appropriations) Bill, the Enacted Budget, and other documents . And that is what budgets are like for many smaller businesses.

For maximum effect, keep the following in mind: 1.

The decision is not either-or but rather how much of each type of approach is appropriate.

This cookie is set by GDPR Cookie Consent plugin. In this article I consider eight managerial concerns in preparing budgets (see the insert for a checklist of these).

Therefore, when the proposed budget is presented, it contains a series of budget decisions that are tied to the attainment of the organization's goals and objectives.

'Top-down'

Several situations call for a top-down approachwhen business unit managers must be given explicit performance objectives because of economic crises, when unit managers lack the perspective to participate in budget setting, and when the nature of the business requires close coordination between units. Budgeting should decide basis for expenditure of funds.

Each operating-unit manager formulates in broad terms the units operating plans, performance targets, and resource requirements.

The most severe criticism is that line item budgeting presents little useful information to decision makers on the functions and activities of organizational units. Budget should harmonise departmental programmes.

What is the difference between ideal and attainable standards? Budgetary Control

Budget should hold back or control unwise expenditure. But companies with a considerable degree of interdependence among operating units need top-down budget guidance for coordination. All rights reserved.

Delegation is something that few owner-managers do well. 5. CIMA Official Terminology 2005 . Each functional executive is asked to prepare and submit the forecast for his department. WebMore commonly, companies use the same document for both purposes.

Budgetary control includes forecasts of income and expenditures (for the budgetary period) on equipment, machinery, manpower, materials, etc., necessary for the efficient production and distribution of estimated volume of sale.

Accelerate your career with Harvard ManageMentor.

9.

Thats why were changing to a rolling budget as of next July 1.. A cyclical process whereby the initial budget formulation is done in broad terms, with details added after everyone agrees on planning assumptions, can be quite effective.

The cycle for companies without a strategic-business-unit (SBU) structure has six steps.

Budgetary control should pin-point those areas which are not working efficiently and according to the predetermined targets.

There is a formal recognition of the targets which the business hopes to achieve.

Web1.2 The budgeting process There are three main elements in the budgeting process, these being objectives, planning and control. In the uncertain atmosphere of start-up companies, the budget might better be related to important actions or events because the organization often takes longer than anticipated to get products perfected, to land the first big order, or to get financing in place.3 In other than start-up situations, budgets are related to time periods in the following way: Large corporations with sophisticated formal planning systems use budgets extensively for controlfirst for coordinating dispersed business units and later, for evaluating units performances. Budgetary control provides a method of control too. Exhibit 3 Actual and Budgeted Performance* (in thousands of dollars), For budgets based on calendar periods, the length of the operating period is usually a month, although smaller companies often prepare budgets for calendar quarters, particularly when they first begin the process. A small company using the top-down approach might initiate the budget process one or two months before the start of the fiscal year, whereas a large company might start six to nine months earlier.

WebDescribe the difference between budgetary planning and control.

Using the budget as a basis for evaluation and compensation is very risky for managers who lack the requisite knowledge.

WebP = budgetary participation, difference scores from mean (P - P) B = budget-emphasis (with +1 for high budget-emphasis, -1 for low) T = task uncertainty, coded difference scores from mean (with +1 for low task uncertainty, and -1 for high).

WebP = budgetary participation, difference scores from mean (P - P) B = budget-emphasis (with +1 for high budget-emphasis, -1 for low) T = task uncertainty, coded difference scores from mean (with +1 for low task uncertainty, and -1 for high). 9. WebEuropean cases expose similarities and differences between political cultures and offer a strong empirical basis to discuss the theories of deliberative and participatory democracy and reveal contradictory tendencies between political systems, public administrations and democratic practices.

From a planning perspective, a budget is the glue that makes the different parts of the organization fit together.

There is also a lot to be said for a corporate culture that encourages unit managers with knowledge of operations and opportunities to put together a realistic budget that takes both long-and short-run considerations into account. Budget is a financial and/or quantitative statement,, , 2. prepared and approved prior to a defined period of time,, , 3. of the policy to be pursued during that period,, 4. for the purpose of attaining a given objective., , Budget is thus a target fixed in For an example of how it works, assume a delivery budget of $1,000 for a sales level of 200 units.

There is also a lot to be said for a corporate culture that encourages unit managers with knowledge of operations and opportunities to put together a realistic budget that takes both long-and short-run considerations into account. Budget is a financial and/or quantitative statement,, , 2. prepared and approved prior to a defined period of time,, , 3. of the policy to be pursued during that period,, 4. for the purpose of attaining a given objective., , Budget is thus a target fixed in For an example of how it works, assume a delivery budget of $1,000 for a sales level of 200 units. Continuous comparison of actual with budgets for achievement of targets.

Copyright 10.

This becomes the so-called current 13-week budget.. In addition to the purposes previously discussedplanning, communicating goals, evaluating performances, and motivating managersbudgets can be used to accomplish three other goals not normally associated with budgeting: delegation, education, and better management of subordinates.

WebBudgetary Control Budgetary control can be defined as a system of controlling costs which includes preparation of budget, coordinating the departments and establishing responsibilities, and comparing actual performance with that budgeted and acting upon results, to achieve maximum profitability or goals (CIMA, 1984). A minority, however, hold out for Budget 1, which seems to them the most reasonable.. Uploaded by Jass Pabla. The more complex the companys products, processes, and environment, of course, the longer the whole process takes.

A good budget is among the best means both for communicating instructions and for evaluating what is being done. Functional executives may take the opinions of Workers, Foreman, Salesman, etc., who remain in direct contact with the job. Some use flexible budgets to evaluate managerial performance while others compare results against original estimates.

This cookie is set by GDPR Cookie Consent plugin.

A participative process takes longer than a top-down budget. The term budget tends to conjure up in the minds of many managers images of inaccurate estimates, produced in tedious detail, which are never exactly achieved but whose shortfalls or overruns require explanations. 2.

As with performance budgeting, program budgeting information may be used to supplement and support traditional budgets in order to increase their informational value. Because this budget presents proposed expenditure amounts only by category, the justifications for such expenditures are not explicit and are often not intuitive. This website uses cookies to improve your experience while you navigate through the website. Operation (Working) of Budgetary Control. In these situations, the knowledge necessary for good budget preparation usually resides at a managerial level one or two steps above that of unit managers.