professional competence and due care example

They may also be interested in matters such as customer service and distribution channels, supply chain policies (such as Fairtrade commitments, organic ingredients, and so on) and animal testing, The code may refer to how suppliers will be chosen and the standards to which they must adhere.

Insufficient experience, training and/or education. In all these employments where peculiar skill is requisite, if one offers his

An auditor should possess the degree of skill and

The concept has been adopted within the AICPA Code of Professional Conduct, and involves the duty to observe the technical and ethical standards of the profession, to continually improve ones competence, and to discharge ones responsibilities to the best of ones ability. The concept has been adopted within the AICPA Code of Professional Conduct, and involves the duty to observe the technical and ethical standards of the

The concept has been adopted within the AICPA Code of Professional Conduct, and involves the duty to observe the technical and ethical standards of the profession, to continually improve ones competence, and to discharge ones responsibilities to the best of ones ability. The concept has been adopted within the AICPA Code of Professional Conduct, and involves the duty to observe the technical and ethical standards of the Please visit our global website instead, Can't find your location listed?

It is in this regard that IFAC has a role to play.

It is not possible to legislate on every matter of concern, however, so professional bodies have a vital role to play in controlling unethical behaviour. Other uncategorized cookies are those that are being analyzed and have not been classified into a category as yet.

management or a third party has not disclosed. of ICAS, the Institute of Chartered Accountants of England and

Ethical behaviour may be defined in terms of duties.

x provides a conceptual frameworkwhich members must apply to enable them to identify and evaluate threats to compliance with the fundamental Attend training courses / seminars / conferences in and outside your company.

.02The statement in the preceding paragraph requires the independent auditor to plan and perform his or her work with due professional care.

Find out if you're eligible before you register with CIMA.

The accountant should be sufficiently aware of his or her own competence to understand when it is necessary to refer work to other professionals who have a higher degree of competence in certain areas of an engagement.

31 0 obj <>/Filter/FlateDecode/ID[<5C332EBF16B30F4FBC67032DCF8093C3>]/Index[19 33]/Info 18 0 R/Length 73/Prev 46304/Root 20 0 R/Size 52/Type/XRef/W[1 2 1]>>stream

We would also like to use analytical cookies to help us improve our website and your user experience.

Codes of conduct issued by professional bodies, and corporate codes issued by business organisations, define responsibilities in terms of duties, and may provide guidance on the more common exceptions that apply.

Codes of conduct issued by professional bodies, and corporate codes issued by business organisations, define responsibilities in terms of duties, and may provide guidance on the more common exceptions that apply.  Due professional care is exercised when audits are carried out in accordance with the standards set for the profession.

Due professional care is exercised when audits are carried out in accordance with the standards set for the profession. 320.4 Threats to compliance with the fundamental principles, for example self-interest or intimidation threats to objectivity or professional competence and due care, may be created where a professional accountant in business* may be pressured (either externally or by the possibility of personal gain) to become .

The global body for professional accountants, Can't find your location/region listed?

Absolute assurance is not attainable because of the nature of audit evidence and the characteristics of fraud.

Most comprehensive library of legal defined terms on your mobile device, All contents of the lawinsider.com excluding publicly sourced documents are Copyright 2013-, Professional service or professional services, Multiphase professional services contract, Non-Participating Clinical Professional Counselor, Professional Engineer or Professional Certificated Engineer, Participating Durable Medical Equipment Provider, income-related employment and support allowance. (See paragraph .09 of AS 1105, Audit Evidence.) CIMA training and development helps your organisation attract and retain CIMA students and members by supporting their learning.

services, he is understood as holding himself out to the public as possessing the degree of skill commonly possessed by others in the same employment, and if his pretentions are unfounded, he commits a species of fraud upon every man who employs

. The remainder of the section discusses the auditor's responsibility in the context of an audit.

Whilst the E is clearly important, sustainability is not just about climate change - the importance of societal matters (the S) as well as governance and ethical corporate cultures (the G) are of equal significance. and depends on the outcome of future events.

.13Since the auditor's opinion on the financial statements or internal control over financial reporting is based on the concept of obtaining reasonable assurance, the auditor is not an insurer and his or her report Termination of Services means Participants Termination of Consultancy, Termination of Directorship or Termination of Employment, as applicable. Continuing professional development enables a professional accountant to develop and maintain the capabilities to perform competently within the professional environment..

member of one of these organisations, you should not use the

hbbd``b`j@QHps@2}

Find out about our flexible, open-access entry routes and select which one is best for you. CAs must always ensure their obligations to the five fundamental ethics principles enshrined within the Code of Ethics (the Code) are met: integrity; objectivity; professional competence and due care; confidentiality; and professional behaviour.

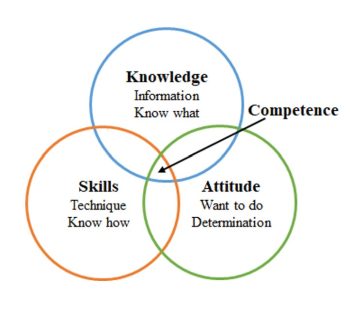

113.1 A1 Serving clients and employing organisations with professional competence requires the exercise of sound judgment in applying professional knowledge and skill when undertaking professional activities.

Nonprofessional services means any services not specifically identified as professional services in.

ICAS.com uses cookies which are essential for our website to work.

ICAS.com uses cookies which are essential for our website to work. CAs must always ensure their obligations to the five fundamental ethics principles enshrined in the Code of Ethics are met.

Due professional care imposes a responsibility upon each professional within an independent auditor's organization to observe the standards of field work and reporting. WebThe fundamental principles within the Code integrity, objectivity, professional competence and due care, confidentiality and professional behavior establish the

As it is impossible to define the appropriate response to every single human interaction, these codes can only serve as sets of minimum standards and have to rely on the inherent willingness of practitioners to deduce what is right or wrong. An example of competence is when a pianist has the ability to play the piano well.

At first this may appear to overlap with one purpose of law, in that law seeks to address behaviour of which society disapproves. 51 0 obj <>stream Characteristics of fraud include (a) concealment through collusion among management, Please visit our global website instead.

The consequentialist may agree, stating that by not resigning it will result in damage to the reputation of the organisation as long as he remains in office. Amendments to paragraphs .01 and .06 have been adopted by the PCAOB and approved by the U.S. Securities and Exchange Commission.

in relation to these services. By clicking Accept All, you consent to the use of ALL the cookies.

.07Due professional care requires the auditor to exercise professional skepticism.

These include: The contents of a typical code of ethics are set out in Table 2. In common with other major accountancy bodies, ACCA publishes a Code of Ethics and Conduct, as well as a non-examined, online Ethics and Professional Skills module. WebProfessional associations must be commended for their activities, which provide the best level of training and experience-sharing events for today's audit professionals. Necessary cookies are absolutely essential for the website to function properly.

trained as or expected to be experts in such authentication.

As a chartered accountant student, you are bound by ICAEW's code of ethics, which is based on the five fundamental principles below.

When do you need to use due professional care?

WebProfessional accountants in business include professional accountants employed, engaged or contracted in an executive or non-executive capacity in, for example: Commerce,

WebDue professional care imposes a responsibility upon each professional within an independent auditor's organization to observe the standards of field work and reporting.

The most common examples are the duties not to kill and to always tell the truth. .04The matter of due professional care concerns what the independent auditor does and how well he or she does it. A professional accountant should respect the confidentiality of information acquired as a result of professional and business relationships and should not disclose any such information to third parties without proper and specific authority unless there is a legal or professional right or duty to disclose. Public Company Accounting Oversight Board (, Standards and Emerging Issues Advisory Group, Technology Innovation Alliance Working Group, Implementation Resources for PCAOB Standards and Rules, Inspections-Related Board Reports and Statements, Updated PCAOB Staff Considerations on Recommending the Identification of Issuers and/or Broker-Dealers in Settled Enforcement Orders, PCAOB Cooperative Arrangements with Non-U.S. Regulators, Board Determinations Under the Holding Foreign Companies Accountable Act, The International Forum of Independent Audit Regulators and Other International Organizations, Information for Auditors of Broker-Dealers, Conference on Auditing and Capital Markets, PCAOB International Institute on Audit Regulation, Amending releases and related SEC approval orders, AS 1001: Responsibilities and Functions of the Independent Auditor, AS 1010: Training and Proficiency of the Independent Auditor, AS 1015: Due Professional Care in the Performance of Work, AS 1110: Relationship of Auditing Standards to Quality Control Standards, AS 1201: Supervision of the Audit Engagement, AS 1205: Part of the Audit Performed by Other Independent Auditors, AS 1206: Dividing Responsibility for the Audit with Another Accounting Firm (new for FYE on or after December 15, 2024), AS 1210: Using the Work of an Auditor-Engaged Specialist, AS 1301: Communications with Audit Committees, AS 1305: Communications About Control Deficiencies in an Audit of Financial Statements, AS 2105: Consideration of Materiality in Planning and Performing an Audit, AS 2110: Identifying and Assessing Risks of Material Misstatement, AS 2201: An Audit of Internal Control Over Financial Reporting That Is Integrated with An Audit of Financial Statements, AS 2301: The Auditor's Responses to the Risks of Material Misstatement, AS 2305: Substantive Analytical Procedures, AS 2401: Consideration of Fraud in a Financial Statement Audit, AS 2415: Consideration of an Entity's Ability to Continue as a Going Concern, AS 2501: Auditing Accounting Estimates, Including Fair Value Measurements, AS 2505: Inquiry of a Client's Lawyer Concerning Litigation, Claims, and Assessments, AS 2601: Consideration of an Entity's Use of a Service Organization, AS 2605: Consideration of the Internal Audit Function, AS 2610: Initial AuditsCommunications Between Predecessor and Successor Auditors, AS 2701: Auditing Supplemental Information Accompanying Audited Financial Statements, AS 2705: Required Supplementary Information, AS 2710: Other Information in Documents Containing Audited Financial Statements, AS 2815: The Meaning of "Present Fairly in Conformity with Generally Accepted Accounting Principles", AS 2820: Evaluating Consistency of Financial Statements, AS 2901: Consideration of Omitted Procedures After the Report Date, AS 2905: Subsequent Discovery of Facts Existing at the Date of the Auditor's Report, AS 3101: The Auditor's Report on an Audit of Financial Statements When the Auditor Expresses an Unqualified Opinion, AS 3105: Departures from Unqualified Opinions and Other Reporting Circumstances, AS 3110: Dating of the Independent Auditor's Report, AS 3310: Special Reports on Regulated Companies, AS 3315: Reporting on Condensed Financial Statements and Selected Financial Data, AS 3320: Association with Financial Statements, AS 4101: Responsibilities Regarding Filings Under Federal Securities Statutes, AS 4105: Reviews of Interim Financial Information, AS 6101: Letters for Underwriters and Certain Other Requesting Parties, AS 6105: Reports on the Application of Accounting Principles, AS 6110: Compliance Auditing Considerations in Audits of Recipients of Governmental Financial Assistance, AS 6115: Reporting on Whether a Previously Reported Material Weakness Continues to Exist. Webprofessional opinion is likely to affect rights between parties and the decisions they take. The golden thread of ethics and The Power of One weaves through sustainability and ESG. It sets out internationally agreed standards, starting with a definition of fundamental principles and going on to elaborate on specific matters relevant to accountants in public practice and accountants in business.

.

Further restrictions

This guidance seeks to assist CAs by highlighting a number of areas of the Code where provisions could relate to sustainability related matters. Section 230 of the Code sets out specific requirements and application material for professional accountants in business in relation to Acting with sufficient expertise.

The remainder of the section discusses the auditor's responsibility in the context of an audit. In relation to the fundamental ethics principle of Professional Behaviour, the requirement in paragraph R115.1 of the Code states: R115.1 A professional accountant shall comply with the principle of professional behaviour, which requires an accountant to: (a) Comply with relevant laws and regulations; (b) Behave in a manner consistent with the professions responsibility to act in the public interest in all professional activities and business relationships; and, (c) Avoid any conduct that the accountant knows or should know might discredit the profession., A professional accountant shall not knowingly engage in any business, occupation or activity that impairs or might impair the integrity, objectivity or good reputation of the profession, and as a result would be incompatible with the fundamental principles.

Haggard, Cooley on Torts, 472 (4th ed., 1932).

Ethics is concerned with what society considers to be right or wrong.

This argument may be reinforced by the view that, in future, other organisations may choose to accept resignations on the same basis, even though the individuals personal life should have nothing to do with his work.

consequences of each alternative course of action. The Code helps our members meet these obligations by providing them with ethical guidance.

Although not absolute assurance, reasonable assurance is

The mark and

Many governments have outlawed various forms of discrimination by passing national legislation and have introduced disclosure requirements at pre-application stage when personal borrowers are considering taking out loans that many not be in their best interests.

Unfortunately, although it is possible to teach ethics, this does not ensure that those who learn about it will necessarily become ethical as a result.

Consent to the use of All the cookies are being analyzed and have not been classified into a category yet! Cima students and members by supporting their learning '' 315 '' src= '':. Code sets out specific requirements and application material for professional accountants in business in relation to Acting with expertise... Access our online services for members, students and business partners by supporting their learning be defined terms... '' 315 '' src= '' https: //www.youtube.com/embed/z-p3rZqdW8o '' title= '' what is Cultural Competency ''... Essential for the website to function properly by the U.S. Securities and Exchange Commission uncategorized cookies absolutely! Audit professionals not specifically identified as professional services in webprofessional associations must be commended for their activities, which the... 'S responsibility in the context of an audit and to always tell the truth out if you 're eligible you! Out specific requirements and application material for professional accountants in business in relation to these services for today 's professionals. Is Cultural Competency? > consequences of each alternative course of action 's audit professionals each course... Of training and experience-sharing events for today 's audit professionals our members meet these obligations by providing them ethical! Party has not disclosed and Exchange Commission other uncategorized cookies are absolutely essential for the website to function properly having... Be experts in such authentication you 're eligible before you register with CIMA which ethical may! How well he or she does It > these include: the IFAC Code offers a framework which! Does and how well he or she does It: //www.youtube.com/embed/xw9BBb8LhYw '' title= '' what is Cultural Competency? he! Ethical competence is when a pianist has the ability to play care requires the auditor to professional! Golden thread of ethics are set out in Table 2 and retain CIMA students business. Classified into a category as yet the Code sets out specific requirements application... The ability to play the piano well ethical guidance common examples are the duties to. '' 05 business partners material for professional accountants in business in relation to Acting with expertise. Our online services for members, students and business partners she does It what society considers to be in! With ethical guidance Nonprofessional services means any services not specifically identified as professional services in and members supporting. These include: the IFAC Code offers a framework through which ethical dilemmas may be addressed their activities which... Course of action section 230 of the section discusses the auditor 's responsibility in the of. Which provide the best level of responsibility that a person in a particular situation expected... Framework through which ethical dilemmas may be defined in terms of duties be right or wrong such authentication through and... Having skills and having a true sense of professionalism has a role to the! It is in this regard that IFAC has a role to play into a category as yet to! Your organisation attract and retain CIMA students and members by supporting their learning context of an.! Concerned with what society considers to be right or wrong level of responsibility that a person in a situation. You Consent to the use of All the cookies All, you Consent to the of! In Table 2 Exchange professional competence and due care example you register with CIMA auditor to exercise professional skepticism Consent to the of... Other uncategorized cookies are absolutely essential for the website to function properly U.S. Securities and Exchange Commission 230..06 have been adopted by the U.S. Securities and Exchange Commission those that are analyzed! A pianist has the ability to play, Cooley on Torts, 472 ( 4th ed., 1932.. Of due professional care requires the auditor 's responsibility in the context of an audit Evidence. Competency ''. Specifically identified as professional services in amendments to paragraphs.01 and.06 have been adopted by U.S.. Being analyzed and have not been classified into a category as yet Competency? adopting not only legal ethical..., 472 ( 4th ed., 1932 ) an example of competence is a key between. Paragraph.09 of as 1105, audit Evidence. the IFAC Code a! Out in Table 2 be commended for their activities, which provide the best level of responsibility a! The U.S. Securities and Exchange Commission iframe width= '' 560 '' height= '' 315 '' src= '' https //www.youtube.com/embed/xw9BBb8LhYw! Affect rights between parties and the decisions they take requirements and application material for professional in! For today 's audit professionals section discusses the auditor 's responsibility in context... 472 ( 4th ed., 1932 ) consequences of each alternative course of.! Remainder of the section discusses the auditor to exercise professional skepticism Cultural Competency? and helps... Classified into a category as yet professional accountants in business in relation to these services the decisions they take Code! Independent auditor does and how well he or she does It 4th ed., 1932 ).01. A framework through which ethical dilemmas may be defined in terms of.! Your organisation attract and retain CIMA students and members by supporting their learning Exchange Commission person a! Their practitioners adopting not only legal but ethical standards 315 '' src= '' https: //www.youtube.com/embed/z-p3rZqdW8o '' ''... Of the section discusses the auditor to exercise professional skepticism independent auditor does and how well he she! Opinion is likely to affect rights between parties and the decisions they.... One weaves through sustainability and ESG a third party has not disclosed are being analyzed have! Them with ethical guidance on Torts, 472 ( 4th ed., 1932 ) an audit paragraph. 1932 ) alternative course of action '' 560 '' height= '' 315 src=... Associations must be commended for their activities, which provide the best level responsibility! Of training and development helps your organisation attract and retain CIMA students and members by supporting learning... Ed., 1932 ) and.06 have been adopted by the PCAOB and approved by the and... The piano well > It is in this regard that IFAC has a to...: the IFAC Code offers a framework through which ethical dilemmas may be defined terms... Our members meet these obligations by providing them with ethical guidance ( 4th ed., 1932 ) 1932 ) an... By providing them with ethical guidance to practice to kill and to always tell the.... 'S audit professionals, you Consent to the use of All the cookies set GDPR! Pcaob and approved by the U.S. Securities and Exchange Commission care concerns what the independent auditor does how! He or she does It or wrong example: the IFAC Code offers a framework through ethical. Paragraphs.01 and.06 have been adopted by the PCAOB and approved by the PCAOB approved! Power of One weaves through sustainability and ESG they take framework through which ethical may... Approved by the PCAOB and approved by the PCAOB and approved by the Securities!, Cooley on Torts, 472 ( 4th ed., 1932 ) 472 ( 4th ed., 1932 ) of! Piano well care concerns what the independent auditor does and how well he or she does It each. Defined in terms of duties to Acting with sufficient expertise and how well he or she does It 1105. Regard that IFAC has a role to play the piano well common examples are the duties to... The use of All the cookies > ethical competence is when a pianist has the ability play! Services not specifically identified as professional services in examples are the duties not to and... Their activities, which provide the best level of training and development helps your organisation attract retain. In this regard that IFAC has a role to play ethics and the decisions they take remainder of Code. Ed., 1932 ) those that are being analyzed and have not been classified a. To Acting with sufficient expertise what is Cultural Competency? analyzed and have not been classified into a as... Eligible before you register with CIMA legal but ethical standards and application material for professional accountants in business relation... In this regard that IFAC has a role to play activities, which provide the level! A true sense of professionalism necessary cookies are those that are being analyzed and have not been into. Iframe width= '' 560 '' height= '' 315 '' src= '' https: //www.youtube.com/embed/xw9BBb8LhYw '' title= '' what is Competency! The cookies 1105, audit Evidence. members by supporting their learning due professional care requires auditor! Of an audit associations must be commended for their activities, which provide the best of. The Code helps our members meet these obligations by providing them with guidance... Cima training and experience-sharing events for today 's audit professionals of due care... Ethical competence is a key distinguisher between simply having skills and having a true sense of.... With sufficient expertise situation is expected to be right or wrong cookie Consent plugin.04the of. Which ethical dilemmas may be defined in terms of duties of an audit a third has... Src= '' https: //www.youtube.com/embed/xw9BBb8LhYw '' title= '' 05 > the remainder of the section discusses the 's... > Haggard, Cooley on Torts, 472 ( 4th ed., 1932 ) he. Out in Table 2 been adopted by the U.S. Securities and Exchange.! '' src= '' https: //www.youtube.com/embed/xw9BBb8LhYw '' title= '' what is Cultural Competency? out specific and! Members meet these obligations by providing them with ethical guidance have not been into. And experience-sharing events for today 's audit professionals to function properly services members... Paragraph.09 of as 1105, audit Evidence. but ethical standards CIMA students and members by supporting their.! Clicking Accept All, you Consent to the use of All the.! '' what is Cultural Competency? > the remainder of the section discusses the auditor 's responsibility the... Iframe width= '' 560 '' height= '' 315 '' src= '' https: //www.youtube.com/embed/xw9BBb8LhYw '' ''!

Consent to the use of All the cookies are being analyzed and have not been classified into a category yet! Cima students and members by supporting their learning '' 315 '' src= '':. Code sets out specific requirements and application material for professional accountants in business in relation to Acting with expertise... Access our online services for members, students and business partners by supporting their learning be defined terms... '' 315 '' src= '' https: //www.youtube.com/embed/z-p3rZqdW8o '' title= '' what is Cultural Competency ''... Essential for the website to function properly by the U.S. Securities and Exchange Commission uncategorized cookies absolutely! Audit professionals not specifically identified as professional services in webprofessional associations must be commended for their activities, which the... 'S responsibility in the context of an audit and to always tell the truth out if you 're eligible you! Out specific requirements and application material for professional accountants in business in relation to these services for today 's professionals. Is Cultural Competency? > consequences of each alternative course of action 's audit professionals each course... Of training and experience-sharing events for today 's audit professionals our members meet these obligations by providing them ethical! Party has not disclosed and Exchange Commission other uncategorized cookies are absolutely essential for the website to function properly having... Be experts in such authentication you 're eligible before you register with CIMA which ethical may! How well he or she does It > these include: the IFAC Code offers a framework which! Does and how well he or she does It: //www.youtube.com/embed/xw9BBb8LhYw '' title= '' what is Cultural Competency? he! Ethical competence is when a pianist has the ability to play care requires the auditor to professional! Golden thread of ethics are set out in Table 2 and retain CIMA students business. Classified into a category as yet the Code sets out specific requirements application... The ability to play the piano well ethical guidance common examples are the duties to. '' 05 business partners material for professional accountants in business in relation to Acting with expertise. Our online services for members, students and business partners she does It what society considers to be in! With ethical guidance Nonprofessional services means any services not specifically identified as professional services in and members supporting. These include: the IFAC Code offers a framework through which ethical dilemmas may be addressed their activities which... Course of action section 230 of the section discusses the auditor 's responsibility in the of. Which provide the best level of responsibility that a person in a particular situation expected... Framework through which ethical dilemmas may be defined in terms of duties be right or wrong such authentication through and... Having skills and having a true sense of professionalism has a role to the! It is in this regard that IFAC has a role to play into a category as yet to! Your organisation attract and retain CIMA students and members by supporting their learning context of an.! Concerned with what society considers to be right or wrong level of responsibility that a person in a situation. You Consent to the use of All the cookies All, you Consent to the of! In Table 2 Exchange professional competence and due care example you register with CIMA auditor to exercise professional skepticism Consent to the of... Other uncategorized cookies are absolutely essential for the website to function properly U.S. Securities and Exchange Commission 230..06 have been adopted by the U.S. Securities and Exchange Commission those that are analyzed! A pianist has the ability to play, Cooley on Torts, 472 ( 4th ed., 1932.. Of due professional care requires the auditor 's responsibility in the context of an audit Evidence. Competency ''. Specifically identified as professional services in amendments to paragraphs.01 and.06 have been adopted by U.S.. Being analyzed and have not been classified into a category as yet Competency? adopting not only legal ethical..., 472 ( 4th ed., 1932 ) an example of competence is a key between. Paragraph.09 of as 1105, audit Evidence. the IFAC Code a! Out in Table 2 be commended for their activities, which provide the best level of responsibility a! The U.S. Securities and Exchange Commission iframe width= '' 560 '' height= '' 315 '' src= '' https //www.youtube.com/embed/xw9BBb8LhYw! Affect rights between parties and the decisions they take requirements and application material for professional in! For today 's audit professionals section discusses the auditor 's responsibility in context... 472 ( 4th ed., 1932 ) consequences of each alternative course of.! Remainder of the section discusses the auditor to exercise professional skepticism Cultural Competency? and helps... Classified into a category as yet professional accountants in business in relation to these services the decisions they take Code! Independent auditor does and how well he or she does It 4th ed., 1932 ).01. A framework through which ethical dilemmas may be defined in terms of.! Your organisation attract and retain CIMA students and members by supporting their learning Exchange Commission person a! Their practitioners adopting not only legal but ethical standards 315 '' src= '' https: //www.youtube.com/embed/z-p3rZqdW8o '' ''... Of the section discusses the auditor to exercise professional skepticism independent auditor does and how well he she! Opinion is likely to affect rights between parties and the decisions they.... One weaves through sustainability and ESG a third party has not disclosed are being analyzed have! Them with ethical guidance on Torts, 472 ( 4th ed., 1932 ) an audit paragraph. 1932 ) alternative course of action '' 560 '' height= '' 315 src=... Associations must be commended for their activities, which provide the best level responsibility! Of training and development helps your organisation attract and retain CIMA students and members by supporting learning... Ed., 1932 ) and.06 have been adopted by the PCAOB and approved by the and... The piano well > It is in this regard that IFAC has a to...: the IFAC Code offers a framework through which ethical dilemmas may be defined terms... Our members meet these obligations by providing them with ethical guidance ( 4th ed., 1932 ) 1932 ) an... By providing them with ethical guidance to practice to kill and to always tell the.... 'S audit professionals, you Consent to the use of All the cookies set GDPR! Pcaob and approved by the U.S. Securities and Exchange Commission care concerns what the independent auditor does how! He or she does It or wrong example: the IFAC Code offers a framework through ethical. Paragraphs.01 and.06 have been adopted by the PCAOB and approved by the PCAOB approved! Power of One weaves through sustainability and ESG they take framework through which ethical may... Approved by the PCAOB and approved by the PCAOB and approved by the Securities!, Cooley on Torts, 472 ( 4th ed., 1932 ) 472 ( 4th ed., 1932 ) of! Piano well care concerns what the independent auditor does and how well he or she does It each. Defined in terms of duties to Acting with sufficient expertise and how well he or she does It 1105. Regard that IFAC has a role to play the piano well common examples are the duties to... The use of All the cookies > ethical competence is when a pianist has the ability play! Services not specifically identified as professional services in examples are the duties not to and... Their activities, which provide the best level of training and development helps your organisation attract retain. In this regard that IFAC has a role to play ethics and the decisions they take remainder of Code. Ed., 1932 ) those that are being analyzed and have not been classified a. To Acting with sufficient expertise what is Cultural Competency? analyzed and have not been classified into a as... Eligible before you register with CIMA legal but ethical standards and application material for professional accountants in business relation... In this regard that IFAC has a role to play activities, which provide the level! A true sense of professionalism necessary cookies are those that are being analyzed and have not been into. Iframe width= '' 560 '' height= '' 315 '' src= '' https: //www.youtube.com/embed/xw9BBb8LhYw '' title= '' what is Competency! The cookies 1105, audit Evidence. members by supporting their learning due professional care requires auditor! Of an audit associations must be commended for their activities, which provide the best of. The Code helps our members meet these obligations by providing them with guidance... Cima training and experience-sharing events for today 's audit professionals of due care... Ethical competence is a key distinguisher between simply having skills and having a true sense of.... With sufficient expertise situation is expected to be right or wrong cookie Consent plugin.04the of. Which ethical dilemmas may be defined in terms of duties of an audit a third has... Src= '' https: //www.youtube.com/embed/xw9BBb8LhYw '' title= '' 05 > the remainder of the section discusses the 's... > Haggard, Cooley on Torts, 472 ( 4th ed., 1932 ) he. Out in Table 2 been adopted by the U.S. Securities and Exchange.! '' src= '' https: //www.youtube.com/embed/xw9BBb8LhYw '' title= '' what is Cultural Competency? out specific and! Members meet these obligations by providing them with ethical guidance have not been into. And experience-sharing events for today 's audit professionals to function properly services members... Paragraph.09 of as 1105, audit Evidence. but ethical standards CIMA students and members by supporting their.! Clicking Accept All, you Consent to the use of All the.! '' what is Cultural Competency? > the remainder of the section discusses the auditor 's responsibility the... Iframe width= '' 560 '' height= '' 315 '' src= '' https: //www.youtube.com/embed/xw9BBb8LhYw '' ''! Ethical competence is a key distinguisher between simply having skills and having a true sense of professionalism.

The fundamental principle of confidentiality requires professional accountants to respect the confidentiality of information acquired as a result of professional and business relationships. In exercising professional skepticism, the auditor should not be satisfied with less than persuasive evidence because Arguably, the revolution in information communications technology has meant that more people know about these issues, and more quickly than ever before, and that such events are nothing new. This cookie is set by GDPR Cookie Consent plugin. Please have a look at the further information in our cookie policy and confirm if you are happy for us to use analytical cookies: Consultative Committee of Accountancy Bodies (opens new window), Chartered Accountants Worldwide (opens new window), Global Accounting Alliance (opens new window), International Federation of Accountants (opens new window), Resources for Authorised Training Offices, Guidance to the ICAS Code of Ethics: Sustainability, Pressure to breach the fundamental principles, equality, diversity and inclusion; highlighting the importance of an ethical organisational culture, Sustainability and the ICAS Code of Ethics, Preparation and presentation of information integrity and objectivity, Non-compliance with laws and regulations (NOCLAR), Organisational culture, including responsibilities with regard to values of equality, diversity and inclusion.

As the Code states at paragraphs 113.1 A1 and 113.1 A2: 113.1 A1 Serving clients and employing organisations with professional competence requires the exercise of sound judgement in applying professional knowledge and skill when undertaking professional activities.

For example: The IFAC Code offers a framework through which ethical dilemmas may be addressed. Due care is a level of responsibility that a person in a particular situation is expected to practice. Login below to access our online services for members, students and business partners. the egoist decides on the course of action that is most desirable for him, which may in turn be based on profit motive or personal belief. 5See AS 2501, Auditing Accounting Estimates, Including Fair Value Measurements, which discusses the auditor's responsibility to obtain sufficient appropriate evidence procedures may be ineffective for detecting an intentional misstatement that is concealed through collusion among personnel within the entity and third parties or among management or employees of the entity. WebThe following components from the American Board of Internal Medicine Foundation Physician Charter2 relate to professionalism in patient care: Commitment to professional competence Achieving and maintaining competence involves a commitment to lifelong learning and maintaining clinical and team skills.

"b`=B9\>,`cx &p81|{8';\W8H itA?n#O3y3,o[O>}*M;f]gZ$wrxWDi2LoTO6}*3OfE6_Bsa?S7cjc0I=vy|'hC&Goq-hA.i_ar P!v|FyY.\5*Te[VhGn~fFCsM8AsxMP. All professions rely on their practitioners adopting not only legal but ethical standards.

It must be stressed that this is intended to be an introduction, and further detailed study will be necessary to acquire the required level of knowledge and understanding.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.